English

English Español

Español 中文

中文

News

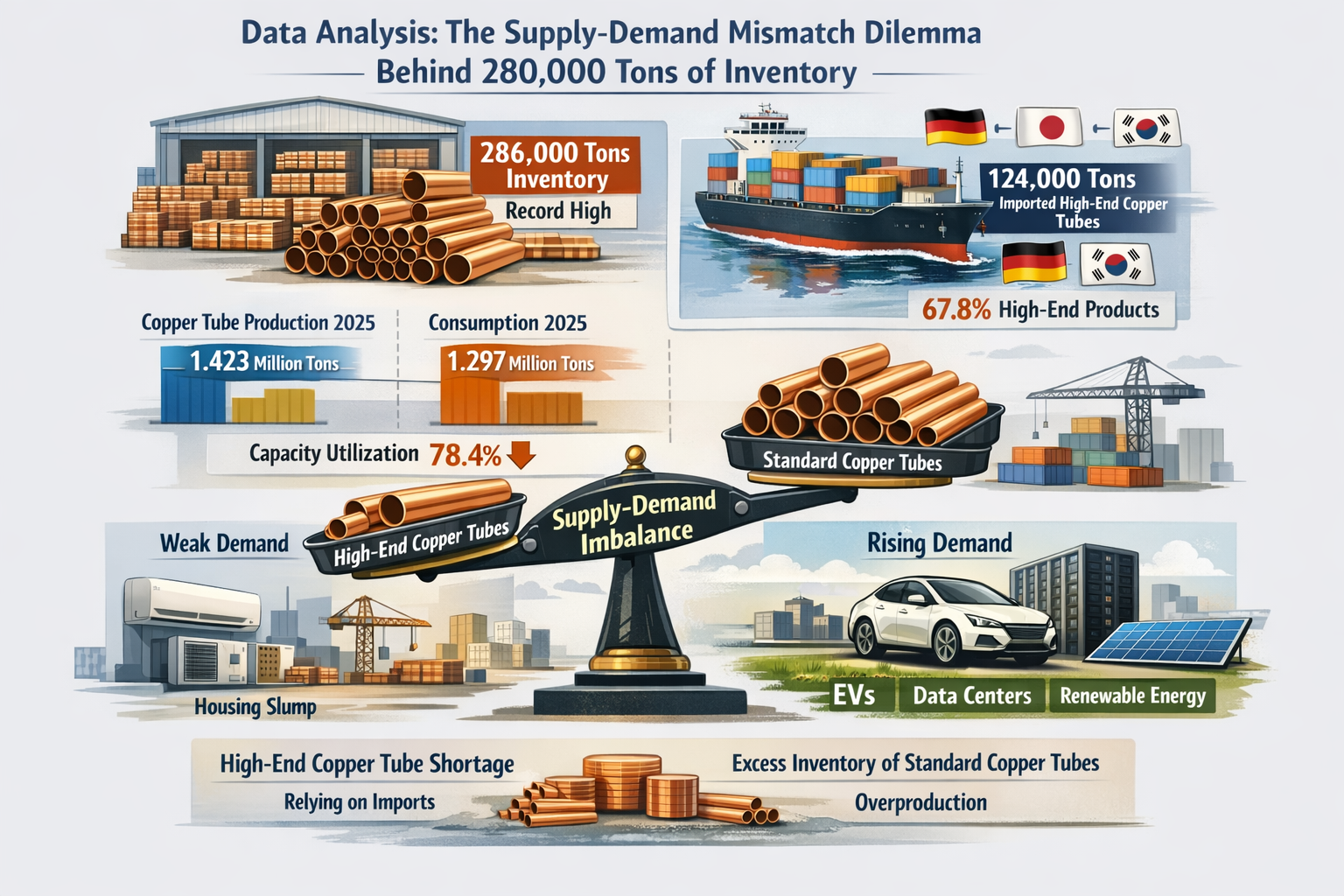

Home / News / Industry News / On one hand, there is a backlog of 280,000 tons of inventory, and on the other hand, there is an annual import cost of $3 billion: When will the “sweet trouble” of China’s copper tube industry be resolved?